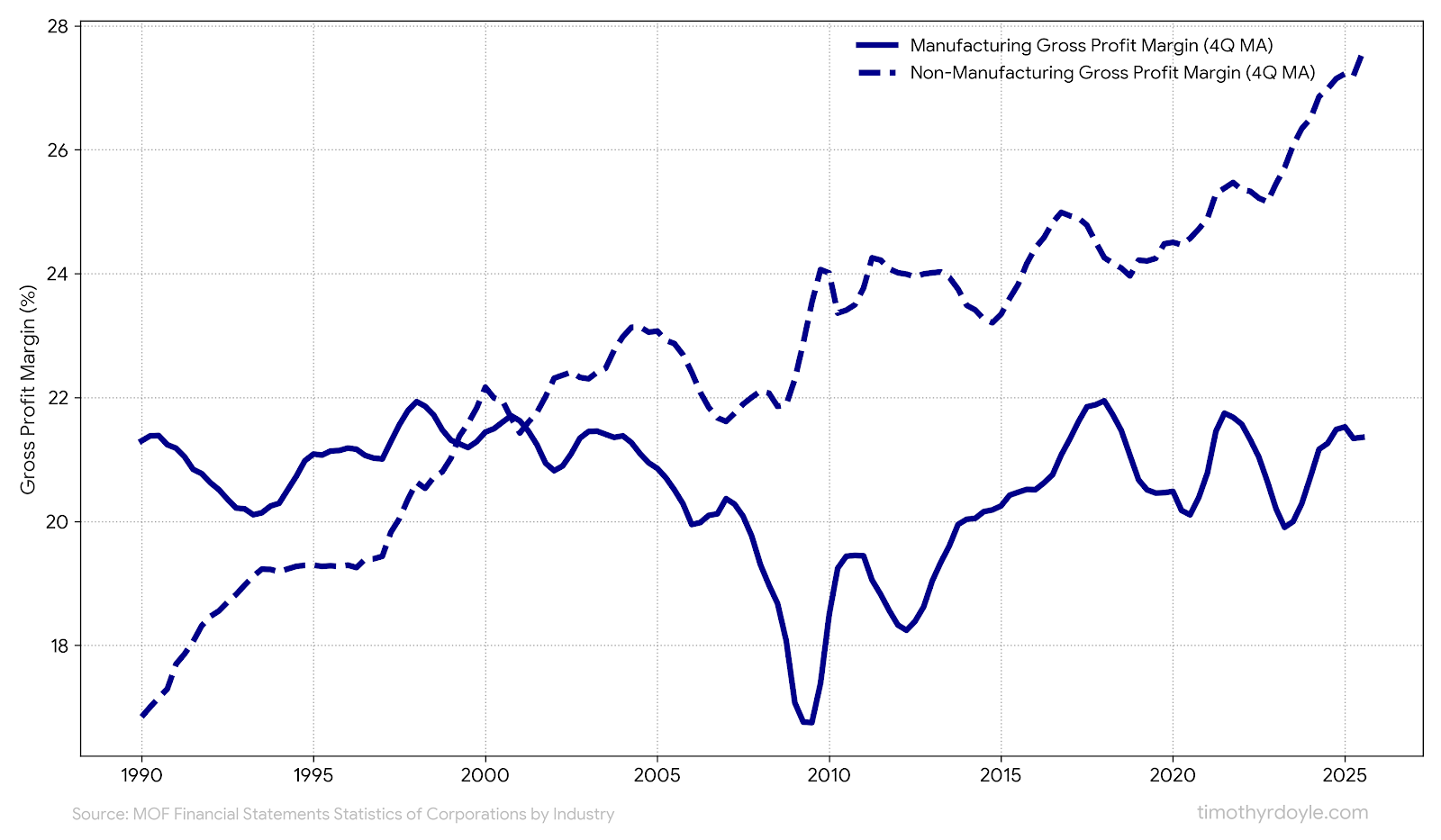

The Profitability Breakout

Many Japanese firms have maintained margins through the current weak yen stress test—proving their pricing power is real. While import costs continue to surge, dominant domestic companies are passing through inflation, revealing which firms have true competitive moats.

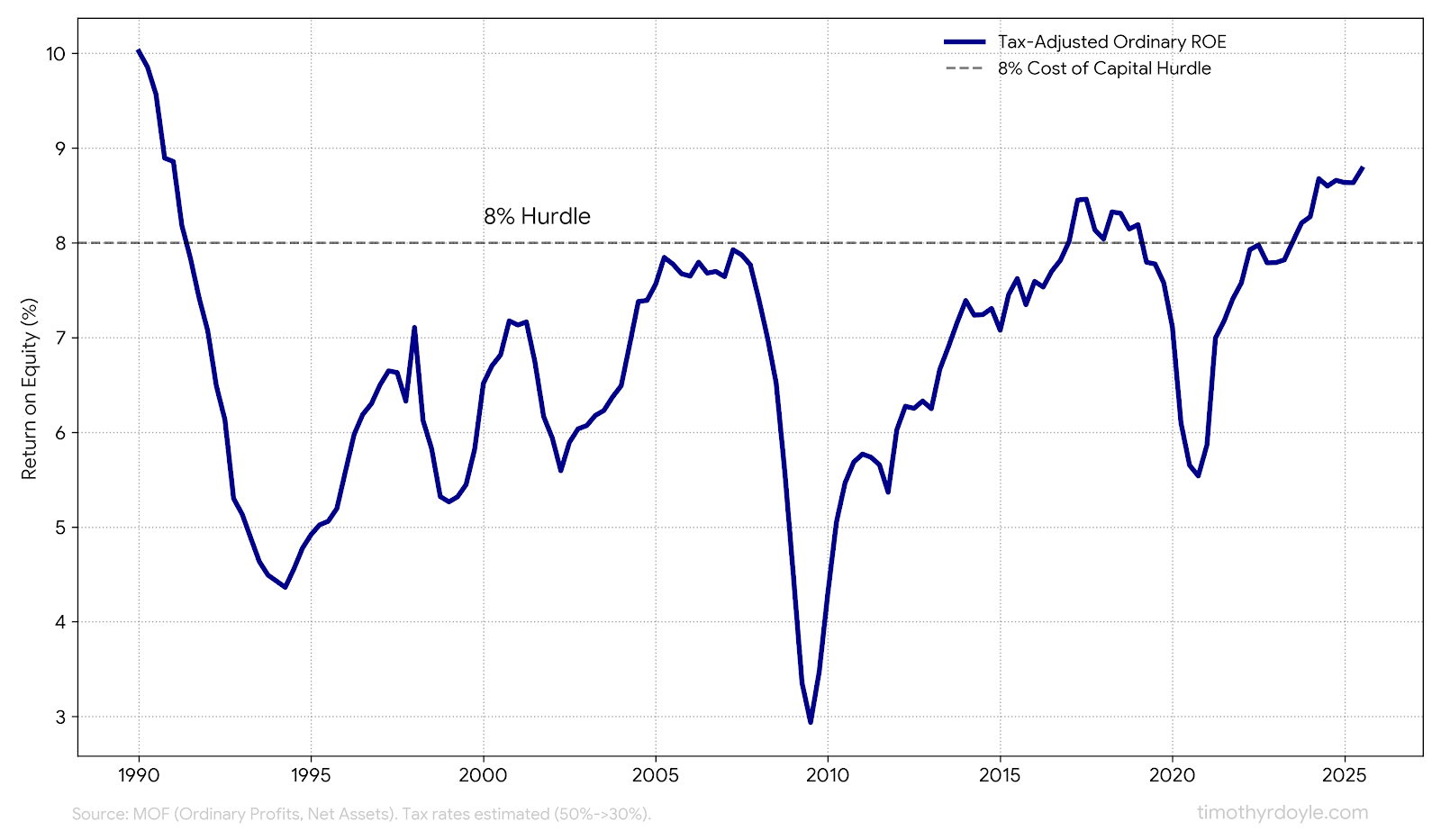

Corporate Japan has finally cleared the 8% ROE hurdle for the first time in decades. This isn’t cyclical—it’s structural. Governance reforms, fortress balance sheets, and automation-driven productivity are creating sustainable value creation.

Unique Analytical Contributions

This research presents data visualizations I have built myself:

🍔 The Big Mac Index — An index developed by The Economist in 1986. The index presents the price of a Big Mac in various worldwide currencies. The price of a Big Mac in yen is currently half of the price of a Big Mac in US dollars, showing intuitively just how much the yen is undervalued relative to the US dollar.

📊 Combined PPP analysis — Two independent measures confirm the yen’s undervaluation. Purchasing Power Parity compares the relative purchasing power of currencies. Both the Penn World Table and the Organization for Economic Co-operation and Development metrics show just how undervalued the yen is in relation to the US dollar at current exchange rates (~160 yen to the dollar).

📈 16 original figures — Every chart built from primary sources (Japan Ministry of Finance, Bank of Japan, US Bureau of Labor Statistics, Organization for Economic Co-operation and Development, The Economist). The paper provides transparency through extensive endnotes for independent verification.

The Investment Opportunity

The macro setup: ¥1,700 trillion in household and corporate liquid savings mobilizing into a ¥1,300 trillion equity market—driven by negative real rates, extreme yen undervaluation, and government incentives and pressure for both corporations and households.

The stock selection thesis: While TOPIX at 19.8x offers limited margin of safety, select domestic firms provide asymmetric upside across three scenarios:

- Weak yen persists → Market share consolidation as sub-scale rivals fail

- Rates normalize → Fortress balance sheets generate offsetting interest income

- Yen mean-reverts → Explosive margin windfall as input costs collapse

The current inflation and weak yen stress test has already revealed which companies can thrive in volatility. The paper provides a framework for identifying them.

Read the Full Paper

📄 Read Full Paper (PDF, 31 pages)

🌐 Read Executive Summary — Detailed summary with additional charts

Published March 2026

About the Author: Timothy R. Doyle is an independent thinker applying multidisciplinary frameworks and mental models to identify where consensus may drift from the underlying reality.